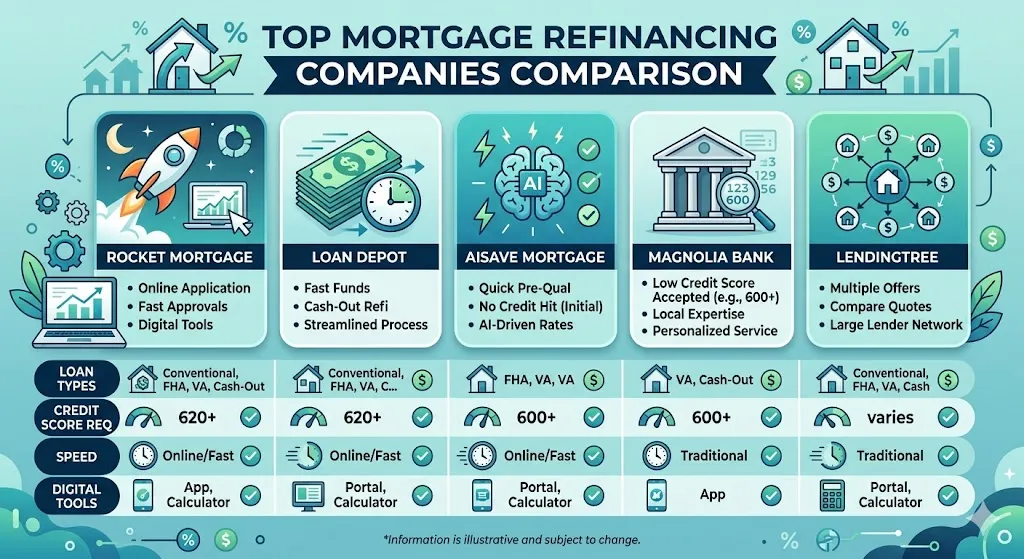

Best Mortgage Lenders in Chicago for 2026

Best Mortgage Lenders in Chicago for 2026

Top Picks at a Glance for Chicago Buyers

Chicago's median home price sits around $320,000 in 2026, meaning most buyers need a loan in the $270,000–$300,000 range — well within conforming limits, but competitive enough that lender speed and fee structure matter a lot.

| Lender | Best For | Min. Credit Score | Min. Down Payment | Rating /5 |

|---|---|---|---|---|

| Rocket Mortgage | Fast online closing | 580 (FHA) / 620 (Conv.) | 3% | 4.8 |

| Better.com | Low fees, rate shoppers | 620 | 3% | 4.5 |

| Chase | Existing bank customers | 620 | 3% | 4.4 |

| loanDepot | First-time buyers, FHA | 580 | 3.5% (FHA) | 4.3 |

| Guild Mortgage | Low credit, niche programs | 540 | 3% | 4.2 |

Why Chicago Buyers Need to Choose Carefully

Chicago's median home price of approximately $320,000 keeps most purchases comfortably under the 2026 conforming loan limit of $806,500 — meaning jumbo loans are rarely needed unless you're buying in Lincoln Park, the Gold Coast, or Lakeview. That said, property taxes in Cook County are among the highest in the nation, which directly affects your debt-to-income ratio and how much lenders will approve you for.

Freddie Mac's April 2026 survey shows the average 30-year fixed rate at 6.28%, and Chicago buyers should focus on lenders with low origination fees rather than chasing fractional rate differences. Closing speed also matters in Chicago's competitive North Side neighborhoods, where well-priced homes still attract multiple offers.

Lender-by-Lender Breakdown

Rocket Mortgage

Rocket Mortgage is the largest retail mortgage lender in the U.S. and is known for its fully digital process that can take a Chicago buyer from application to clear-to-close in as little as 8 days. For a city where North Side inventory moves fast, that speed is a genuine advantage.

- ✅ Best for: Chicago buyers who need a quick pre-approval letter for competitive offers

- ✅ Min. credit score: 580 (FHA), 620 (Conventional)

- ✅ Min. down payment: 3%

- ✅ Avg. closing time: 26–30 days

Pros: Industry-leading digital experience; accepts lower credit scores on FHA products.

Cons: Origination fees can run higher than online-only competitors; no in-person branches in Chicago.

Better.com

Better.com operates as a fee-transparent online lender with no origination fees and no commissions — a strong fit for rate-conscious Chicago buyers who have already done their research. According to the CFPB, comparing at least three lenders before committing can save borrowers thousands over the life of a loan, and Better makes that comparison easy.

- ✅ Best for: Chicago buyers with strong credit who want to minimize closing costs

- ✅ Min. credit score: 620

- ✅ Min. down payment: 3%

- ✅ Avg. closing time: 21–32 days

Pros: No lender fees; instant online rate quotes without a hard credit pull.

Cons: No FHA or USDA loans; customer service is fully remote, which can frustrate buyers who want local guidance.

Chase

Chase has a strong brick-and-mortar presence across Chicago with dozens of branches, making it a natural fit for buyers who want face-to-face guidance. Existing Chase checking or savings customers may qualify for closing cost discounts through the bank's relationship pricing program.

- ✅ Best for: Chicago buyers who already bank with Chase and want in-person support

- ✅ Min. credit score: 620

- ✅ Min. down payment: 3% (DreaMaker loan)

- ✅ Avg. closing time: 30–40 days

Pros: Local branch access throughout Chicagoland; relationship discounts for existing customers.

Cons: Online process is slower than fintech lenders; rates are sometimes less competitive for non-Chase customers.

loanDepot

loanDepot is one of the country's largest FHA lenders and a solid choice for first-time Chicago buyers who don't have large down payments saved. FHA guidelines require just 3.5% down with a 580 credit score, and loanDepot's loan officers are well-versed in pairing FHA financing with Illinois down payment assistance programs.

- ✅ Best for: First-time Chicago buyers using FHA loans or Illinois IHDA assistance

- ✅ Min. credit score: 580

- ✅ Min. down payment: 3.5% (FHA)

- ✅ Avg. closing time: 28–35 days

Pros: Strong FHA expertise; familiar with Illinois Housing Development Authority (IHDA) grant programs.

Cons: Website and digital tools are less polished than Rocket or Better; rate transparency requires a full application.

Guild Mortgage

Guild Mortgage specializes in borrowers with thin credit files or non-traditional income — a good fit for Chicago buyers who are self-employed, newer to credit, or recovering from past financial setbacks. They accept credit scores as low as 540 on certain FHA products, which is notably lower than most national lenders.

- ✅ Best for: Chicago buyers with credit scores below 600 or complex income situations

- ✅ Min. credit score: 540

- ✅ Min. down payment: 3%

- ✅ Avg. closing time: 30–40 days

Pros: Lowest credit score threshold among major lenders; strong niche and down payment assistance program knowledge.

Cons: Not available in all Illinois zip codes; fewer digital tools compared to Rocket or Better.

Side-by-Side Comparison

| Lender | Rate Type | Origination Fees | Online Process | Best For | Min. Score |

|---|---|---|---|---|---|

| Rocket Mortgage | Fixed & ARM | ~1% of loan | Fully online | Speed, competitive offers | 580 |

| Better.com | Fixed & ARM | $0 | 100% digital | Low fees, rate shoppers | 620 |

| Chase | Fixed & ARM | Varies (discounts available) | Hybrid (branch + online) | Existing customers, in-person | 620 |

| loanDepot | Fixed & ARM | Varies by loan type | Partial online | FHA, first-time buyers | 580 |

| Guild Mortgage | Fixed & ARM | Varies | Partial online | Low credit, niche programs | 540 |

Which Lender Is Right for You in Chicago?

- If your credit score is 720+: Better.com — no origination fees means you keep more cash at closing on a Chicago home, and your strong credit will qualify you for their best rates without needing hand-holding.

- If you're a first-time buyer: loanDepot — their FHA expertise and knowledge of Illinois IHDA down payment assistance programs makes them especially useful if you're buying your first Chicago home with limited savings.

- If you're buying a high-value Chicago home (over $700k): Chase — their jumbo loan products and relationship pricing work well for buyers in premium Chicago neighborhoods, and a local branch officer can walk you through larger, more complex transactions.

- If your credit score is below 600: Guild Mortgage — their 540 minimum and willingness to work with non-standard income documentation makes them the most accessible option for Chicago buyers rebuilding credit.

- If you want 100% online: Rocket Mortgage — no lender in this list matches their digital speed or pre-approval turnaround, which matters when you're competing for a well-priced home in Wicker Park or Logan Square.

How to Apply for a Mortgage in Chicago — 4 Steps

- Check your credit score and DTI first. Pull your free credit report at AnnualCreditReport.com and calculate your debt-to-income ratio. Chicago's high property taxes mean lenders will scrutinize your DTI carefully — aim for 43% or below before applying.

- Get pre-approved with at least two lenders. A pre-approval letter shows Chicago sellers you're serious. According to the CFPB, comparing two or more Loan Estimates side by side is the clearest way to identify which lender is actually cheaper after all fees are counted.

- Lock your rate once you're under contract. At 6.28% APR on a 30-year fixed (Freddie Mac, April 2026), a rate lock of 45–60 days protects you through Chicago's typical 30–45 day closing timeline.

- Submit final documents and clear underwriting. Have your last two pay stubs, two years of tax returns, and two months of bank statements ready. Chicago co-op buyers should also have the building's financials on hand — underwriters will request them.

Before You Apply — Read These First

Ready to Find Your Chicago Mortgage?

Pick one lender above and check your rate online — it takes less than 5 minutes and does not affect your credit score. Once you have a real rate in hand, you'll know exactly what you can afford in Chicago's market.